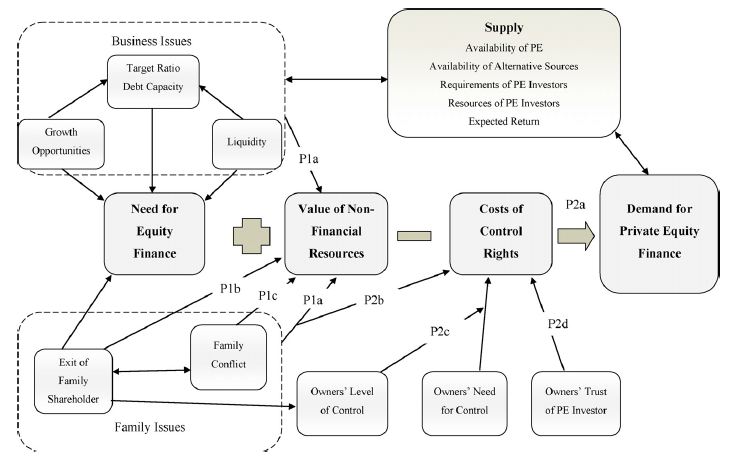

Most family owned businesses survive through the ingenuity, hard work, and resourcefulness of the founder(s) in the first generation. As the founders grow older and the business hits certain barriers to growth, often there is a need for a capital infusion to satisfy the goals of the founders and the other stakeholders in the continued growth and success of the business. Private equity, while a viable option for many privately owned businesses, can be perceived as a solution that is unworkable for the typical family owned business because of the fear of loss of control. In an article last year in the Journal of Family Business Strategy (Volume 3, Issue 1, Pages 38-51, March, 2012), authors Florian Tappeiner, Carole Howorth, Ann-Kristin Achleitner, and Stephanie Schraml describe some research they performed on a group of family firms in Germany. The research focused on issues these firms faced in soliciting private equity investment. Excerpts are provided below, along with a diagram, and accompanied by some commentary:

Under the pecking order hypothesis, private equity is a finance of last resort. Tests of the pecking order and its assumptions have provided conflicting results. For family firms, the pecking order hypothesis is incomplete because it ignores family effects. Case studies of 21 large family firms in Germany are analysed. Testable propositions are derived. Family firm owners balanced financial and non-financial resources of private equity with the need to cede control rights. Non-financial resources were valued more highly when resolving family issues. The observed pecking order was driven by control rights. Important implications for family firms and investors are discussed.

The authors articulate that private equity is perceived as a final option for owners of family businesses. No surprise there. Control is seen as the most important factor in determining what outside resources to enlist. Private equity is seen as less widely used than non-financial resources when the goal is to resolve family issues.

Family and business influences are equally important in terms of the demand for private equity in large family owned firms. Private equity was sought out for reasons that included the exit of a sibling, parents’ wealth diversification and business growth. The authors note an “interdependence of demand and supply in financing decisions, most noticeably in the negotiation of control rights, which featured strongly in the interviews. (Sometimes the underpinning reason for seeking an investor was to consolidate control, for example, buying out a family member with conflicting views or concentrating ownership in one branch of the family, which, it was argued, would free up decision making within the family firms.)”

Minority private equity investments provided study participants with needed finance while allowing the family owners to maintain family control. Private equity also provides managerial resources. The presence of outside money and potential ensuing leverage in executive decision making illustrates the potential for better corporate governance practices and enhanced expertise to pursue business opportunities, such as IPOs or globalization. Said the authors, “Firms with family issues may value the non-financial resources that private equity investors may provide. In particular, family firms wishing to reduce family conflicts may value the neutral or professional role of a private equity investor.”

It was noted that business performance issues led to loss of control in two of the family firms receiving private equity infusions. Still others negotiated control rights guidelines aggressively because of their concerns over the potential of such an occurrence. The investors, for their part, acknowledged that dealing with family firms presented a unique set of challenges usually not experienced in other deals.