According to Bill Warner, co-founder of EntreDot, approximately 26,000 new companies are formed each year in North Carolina and, in that same year, over 23,000 companies fail due to poor management and operational mistakes. Warner further states that, “The statistics are worse in rural and minority populations. This means that good ideas go to waste along with the grant and investor funds that helped get these companies started. As a result, the potential growth of revenue and new jobs is lost also.” These comments are very similar sentiments to what Dun and Bradstreet found in some surveys conducted during the period of 2007 – 2010. D&B found that the rate of business failure went up by an average of 40% during the recession years.

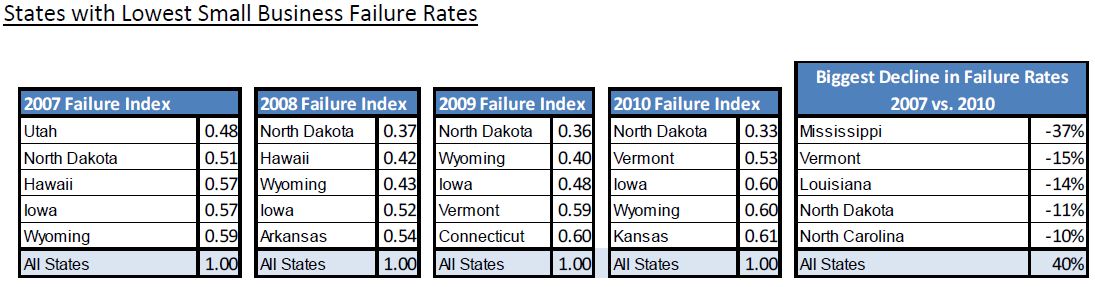

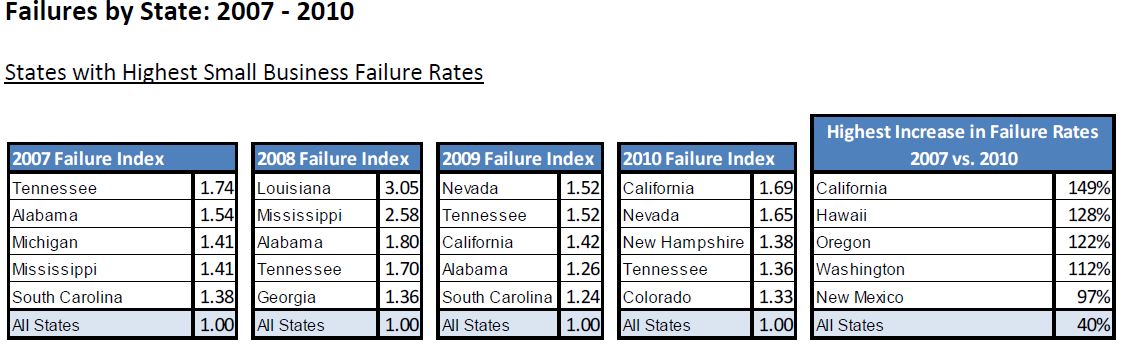

Many of the states with lower failure rate increases are less heavily populated states. In fact, of all the states that have seen a decline in the rate of small to medium sized business failure, only North Carolina makes the list of 10 most populous states in the country. Of states (below) with large increases in failure rates, only California is heavily populated.

From 2007 through 2010, Western states in the West had the highest increase in failure rates. Reasons D&B provided for the uptick in failures include continued instability in the residential housing market and drop-off in the tourism, travel and hospitality sectors. Interestingly, Tennessee has been home to the highest small business failure rates for four years in a row.

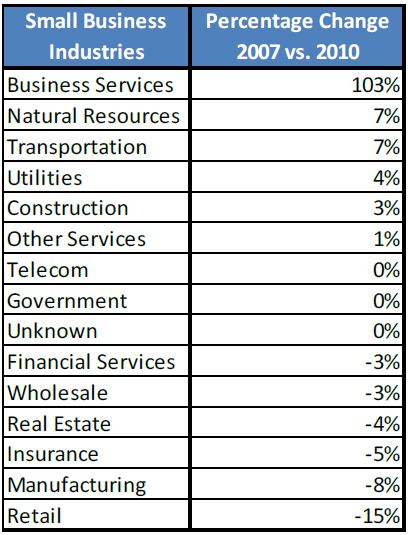

These trends have been occurring at a time when the number of retail establishments and corresponding retail employment have both dropped by 15-20%. On the other hand, the number of SMBs in the Business Services category more than doubled and these businesses experienced a 30% increase in the number of people they employ. The fastest growing industries for SMBs are summarized below:

As you can plainly see, nothing else comes close to the growth of the Business Services category. Bear in mind that many software as a service companies are part of this category and have been launched in only recent years. The macrotrends that become evident are that retail is on the wane, highly populated states are more stable in terms of business failure statistics, and the business services category’s growth will be a key cog in the engine of our economy.

Warner points to the following issues of significance to these small businesses:

- Business strategy and planning to make sure their business is focused on a viable market with a winning product and/or service that has a competitive edge

- Forecasting and financing ensuring that sales forecasts are realistic and that revenue, cost, expense and cash are well managed

- Operational discipline and judgment to increase the chances of success by making fewer mistakes

- Industry connections that can help accelerate the business and its operations

- Start-up company experience that can instill the wisdom of what it takes to really start and manage an emerging business

He feels that these companies need the dual combination of basic business know-how and mentoring. The situation in North Carolina, where Warner and I live, is that our state has a comprehensive array of entrepreneurship education programs throughout the community college and university systems including various other private and public organizations. The problem is that we have little help for entrepreneurs once they have completed these programs and actually try to start a business. We recommend assistance for entrepreneurs who are struggling to create successful businesses, the failures should decline considerably. Entrepreneurs should be seeking out business mentors that can help them through the early years of their business.