In an article last month entitled, “Can Entrepreneurship Be Taught?,” two sides of the argument were presented that, while equally valid, were at odds with one another. Noam Wasserman, Harvard Business School professor of Entrepreneurship and author of “The Founder’s Dilemmas: Anticipating and Avoiding the Pitfalls That Can Sink a Startup,” takes the position that too many founders have to climb the same steep learning curve as others before them, bereft of insights that could help great ideas become great businesses. Victor Hwang, co-author of “The Rainforest: The Secret to Building the Next Silicon Valley” and managing director of T2 Venture Capital in Silicon Valley, posits that only experience can teach an entrepreneur how to successfully launch a business.

Within the Wasserman camp are educators who believe that documented best practices and potential problem areas can be shared with the entrepreneurs. For instance, the idea that the founder must do the three following things has been challenged with research data to instruct otherwise:

- Following one’s gut

- Having a “glass half full” view about resources and time

- Stay in the top executive role as the company matures

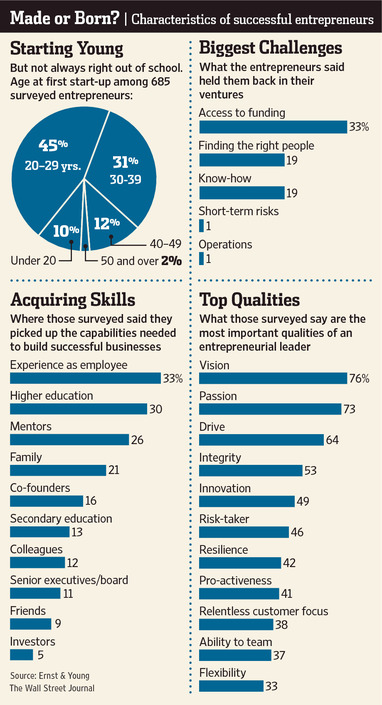

Augmenting the classroom instruction with deliberate opportunities to “try out” a principle in a role play seem to yield good results. Additionally, self assessments are helpful in increasing one’s self awareness and ability to lead others. Notably mentoring is recognized as one of the best ways an entrepreneur can learn how to do the right thing in a myriad of scenarios.

What is also being learned is the need to not just offer principles of management (regardless the field of management–finance, operations, marketing, etc), but to also focus on the soft skills requisite to be an effective leader. Whether the entrepreneur is embracing better social skills, motivational techniques for self and others, or other facets of emotional intelligence, there are competencies to be gained that are simply not intuitive for most.

Hwang and the experiential learning community holds steadfastly to the conviction that entrepreneurship is taught rather than caught and is more of an impartation than an education. Rather than the typical domain of business schools–resource allocation and risk management, it is argued that the necessary skills fall more into the following categories:

- Comfort with a high degree of uncertainty

- Willingness to become a generalist rather than a specialist

- Abilities in inspiring others through storytelling and personal charisma

Since some programs are heading in the direction of trying to advise start-ups on what actions to avoid, Hwang is concerned that the willingness to try something unconventional may become minimalized. He and others believe that such a mindset is critical to entrepreneurial success. The main thesis behind Hwang’s proposed approach is that entrepreneurs would have the greatest chance of success if communities with resources, counsel and mentoring were available for their growth and development.

The common theme, then, is that mentoring and nurture is the best medicine for someone who “suffers” from entrepreneurial dreams. We wholeheartedly concur with this bottom line approach and advocate innovation centers (incubators with assigned mentors, education, and planned activities to build a sense of community) as a best practice!